Why do trusts have to be registered using the New UK Trust Registration Service?

HM Revenue and Customs (HMRC) accepted registration of trusts with paper form 41G (Trust) until April 2017 and the new UK Trust Registration Service is a replacement online trust registration procedure, enabling trustees to maintain trust records.

The opportunity has been taken by HMRC to allow executors a registration procedure for ‘Complex Estates’.

A secondary purpose of the Trust Registration Service is for the Government to meet the EU Fourth Money Laundering directive by compiling and sharing a list of the beneficial owners of trusts. The details of the trust, trustees, beneficiaries, and influencers may be accessed by other fiscal and policing authorities although the register is not currently available to the public.

How to register a trust online.

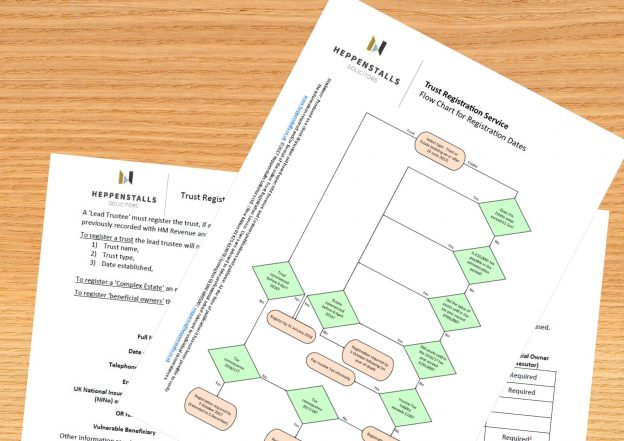

The first of the requirements for trust registration is for trustees and executors to determine if a particular trust or estate actually requires registration. There are various factors to determine the requirements for trust registration, largely depending upon whether tax is payable in a particular tax year or during the administration of a complex estate. Heppenstalls Solicitors have developed a helpful PDF flowchart to guide our Clients, trustees, executors and beneficiaries which can be viewed here to determine if and when online trust registration is required.

Registering a trust with HMRC on the UK trust register requires a ‘lead’ trustee to obtain a Government Gateway account and to collate significant facts about the trust or estate, and personal identifying information for beneficiaries, trustees, influencers or executors. Heppenstalls Solicitors have developed a helpful PDF introductory guide to trust registration documents for our Clients, trustees, executors and beneficiaries which can be viewed here to help identify the requirements and documents required for the trust registration process.

The trust registration act requires trustees to collect, record and maintain this information, even if the trust is not registerable, and to keep these records for at least five years. Private trustees need to consider whether registration with the Information Commissioner’s Office is required.

How to apply for trust registration.

The application form for new trust registration is interactive and the Government HMRC portal showing where to register a trust is here

Registration of your trust or estate cannot be undertaken by agents until HMRC provide access shortly.

If you would like Heppenstalls Solicitors to assist with trust or estate problems, please let us know at contact us, or email enquiries@Heppenstalls.co.uk or contact our experts on 01425 610078 for Steven Lord or 01590 689500 for Mrs Jennings.

- November 2022

- September 2022

- August 2022

- July 2022

- March 2022

- November 2021

- February 2021

- December 2020

- September 2019

- June 2019

- May 2019

- April 2019

- February 2019

- January 2019

- September 2018

- August 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- October 2016

- September 2016

- April 2016

- February 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014